Growing liquidity risk in fixed income portfolios

Liquidity, like the plumbing in your house, gets little attention until something goes wrong.

Across the fixed income asset class, core government bonds sit at the most reliably liquid end of the spectrum, with liquidity then progressively decreasing for credit-risky securities such as corporate bonds, emerging market debt, loans and securitised investments, all of which can become hard to buy or sell, particularly in adverse market environments.

To be clear, illiquid securities are not inherently bad. They can be attractive when liquidity risk is explicitly recognised, well compensated and the time horizon of capital is appropriate.

Problems arise when liquidity risk is hidden and creeps into portfolios that are expected to remain liquid and intended to play a defensive role.

In our view, the following themes can’t be ignored.

- Hidden liquidity risk

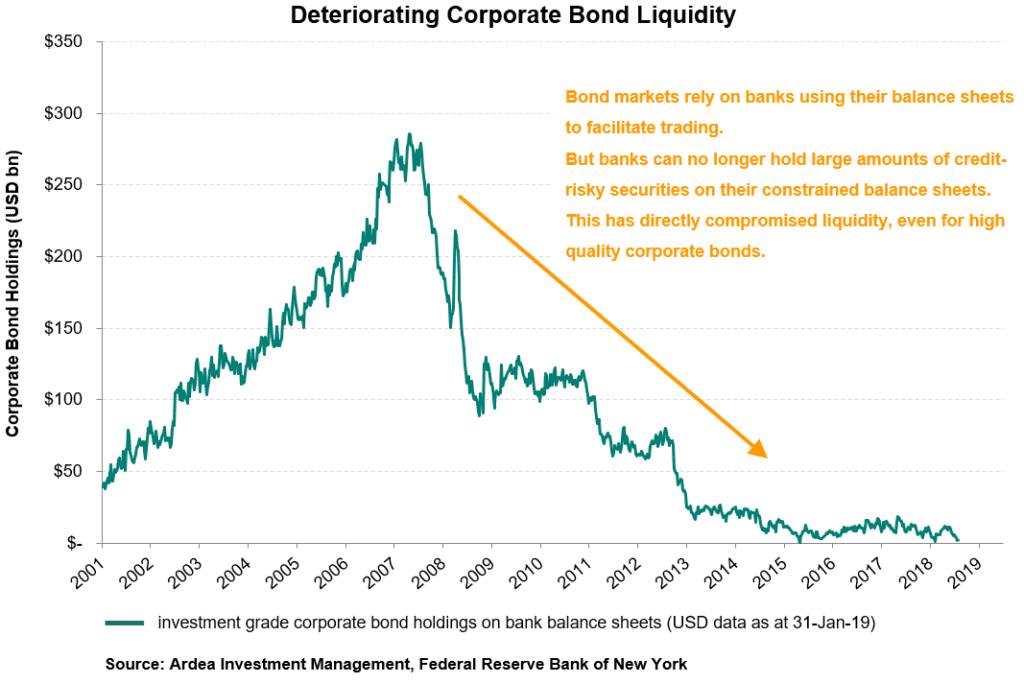

Liquidity in credit-risky segments of fixed income has deteriorated due to bank balance sheet constraints. (see chart below)

This hasn’t yet been obvious because the sheer volume of yield chasing inflows to credit markets has provided an illusion of liquidity. It’s only when the inflows turn to outflows that the reality of illiquidity will become clear.

- Illiquidity creep

With interest rates collapsing globally, investors are under intense pressure to find ways to boost returns. As a direct result of this, portfolio allocations to higher yielding, but less liquid bonds and loans has been creeping higher.

Most vulnerable to a future liquidity crunch are those running a growing mismatch between the regular liquidity they promise investors and the illiquidity of their underlying investments.

We expect to see more liquidity related problems surface as the desperate search for yield compels ostensibly liquid portfolios to keep pushing the limits. (examples here, here and here)

These articles provide more detail:

Ardea IM Insights – Hidden liquidity risk in FI portfolios

Ardea IM Insights – Are illiquid bonds the WeWork of the FI world?