The Three Levers in Fixed Income: Duration, Credit and Pure Relative Value

“In a world that is constantly changing, there is no one subject or set of subjects that will serve you for the foreseeable future, let alone for the rest of your life.” – John Naisbitt, an American author, whose analysis of social trends led to predictions regarding automation in the workplace, globalisation and even the rise of artificial intelligence. While some of his predictions were a little wide of the mark, this quote about change can certainly be applied to the world of investing and the current macro environment where predicting the future level and direction of interest rates is inherently difficult.

Adding Pure Relative Value upgrades the portfolio diversification toolkit

Within Fixed income, there are two well-known levers, duration and credit. In addition, there is also a lesser known third lever, Pure Relative Value investing. This third lever provides compelling diversification benefits when blended with duration and credit.

Ultra-low inflation and zero interest rates to sky-high pricing and aggressive tightening

Investors have faced tremendous change over the past decade and perhaps an even more radical shift in recent years as ultra-low inflation and zero, even negative, interest rates gave way to sky-high pricing and aggressive tightening by central banks in both the developed and emerging world. Rapidly rising interest rates have been particularly painful for fixed income investors but have also contributed to equity market uncertainty and created dislocations in the relationship between asset classes.

Central banks become volatility amplifiers

Central banks have suffered some criticism for their response to the challenge of rising inflation and dwindling economic growth and while some of this may be unfair, central banks in fixed income markets have undeniably shifted from suppressors of market volatility to volatility amplifiers.

Until recently, central banks were quick to intervene whenever there was some form of market stress, either in the shape of interest rate cuts or quantitative easing, and that intervention was easy to justify given their objectives of price stability and economic growth were perfectly aligned. Inflation was running well below target, so whatever policy makers did to facilitate stable prices was consistent with supporting growth. These objectives are now misaligned, with the options available to tame inflation undesirable from the perspective of economic prosperity.

Why is this relevant? Bond yields in a structurally higher volatility regime

These conflicting objectives, the associated policy uncertainty and central banks aggressively running down their pandemic-era bond portfolios are why we consider the worlds’ reserve banks to be amplifiers of volatility. This also means that interest rates and bond yields are in a structurally higher volatility regime than they have been for most of the post Global Financial Crisis era (since 2008).

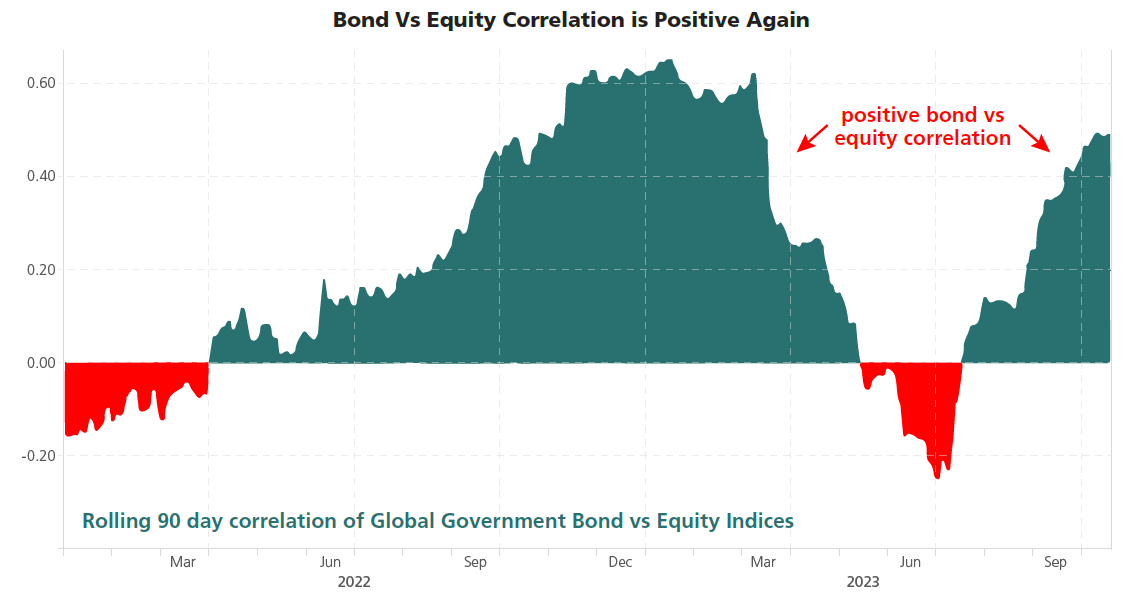

Furthermore, uncertainty about inflation and the path of interest rates introduces a more variable correlation between bonds and equities. This is particularly relevant for multi-asset portfolio managers because the composition of their fixed income allocations now carries more weight. Historically, investors could simply rely on duration (government bonds) to diversify equity risk, but today that duration component is more volatile and also has a more volatile relationship with equities.

Fixed income investors face a similar dilemma, with corporate bonds suffering the same upward pressure on yields (downward pressure on prices) as government issued debt, but with greater potential for default. This means the two traditional levers of fixed income portfolio management – duration and credit – have more uncertainty.

Pure Relative Value (RV) investing

Pure RV investing does not rely on conventional fixed income sources of return and is not impacted by the level of bond yields regardless of whether they are high, low, or even negative. Nor is it reliant on corporate credit risk or a fund managers’ ability to forecast the direction of interest rates. Instead, the Pure RV approach focuses on pricing inconsistencies between closely related securities – it offers investors an additional lever.

The global fixed income market contains a huge array of securities that are explicitly linked to each other by well-defined relationships. In an efficient market, these securities would always be consistently priced with one another, but the fixed income market is not efficient. Underlying structural factors such as regulation, mandate restrictions and varying investor use objectives cause market participants to transact for reasons other than profit maximisation.

As such, we continually observe pricing inconsistencies between closely related securities that have very similar risk characteristics. These pricing inconsistencies can be isolated using a wide range of risk management tools, including derivatives, which strip out unwanted market risk allowing the strategy to target the generation of positive returns regardless of the level of bond yields or the direction of interest rates.

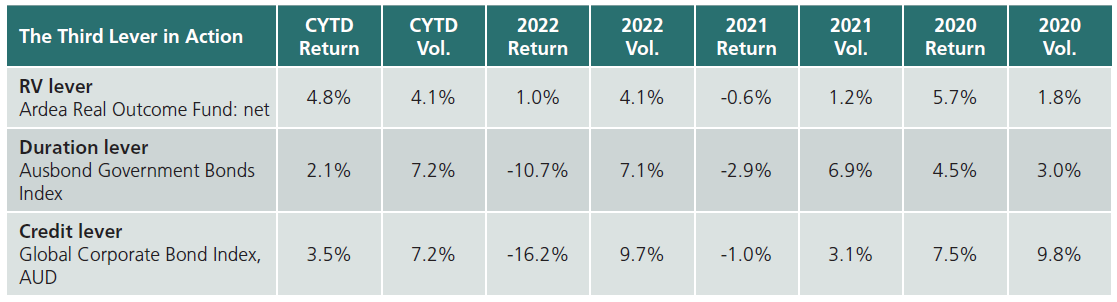

The Ardea Real Outcome Fund (‘ARO’ or ‘Fund’) is an absolute return fund that focuses on Pure RV opportunities within the highest quality and most liquid government bond markets. Our approach is duration neutral and excludes corporate credit, which provides investors a true alternative to traditional fixed income strategies. This additional lever in fixed income provides compelling diversification benefits when blended with the conventional levers of duration and credit and can upgrade the portfolio diversification toolkit as seen in the following table and charts.

Fixed Interest levers in action

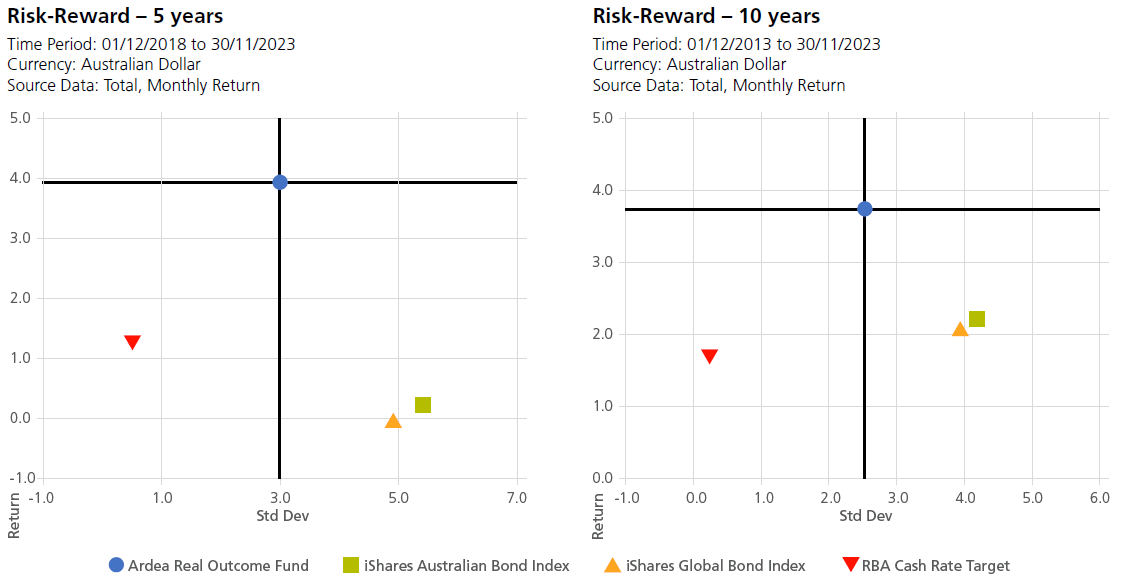

Return target and ‘style of returns’

The Fund targets a medium term return above CPI (inflation), as well as cash, of +2% before fees, it also seeks to deliver uncorrelated investment performance whilst maintaining a modest level of volatility targeted at 2% pa while providing daily liquidity. As such, we consider the style of our returns every bit as important as the size of our returns.

This ‘style of returns’ is illustrated in the following chart from Morningstar direct, it plots cumulative performance against standard deviation for ARO and the core defensive asset allocations – RBA cash, the Bloomberg Ausbond Composite Bond Index and the Bloomberg Global Aggregate Index for 5 years and 10 years to 30 November 2023 (as represented by the iShares index ETFs which replicates the Bloomberg Ausbond Composite Index and the Bloomberg Global Aggregate index.). Since the Fund’s launch*, its RV strategy has outperformed the key fixed income indices included in the analysis, and it has done so with a much lower degree of volatility.

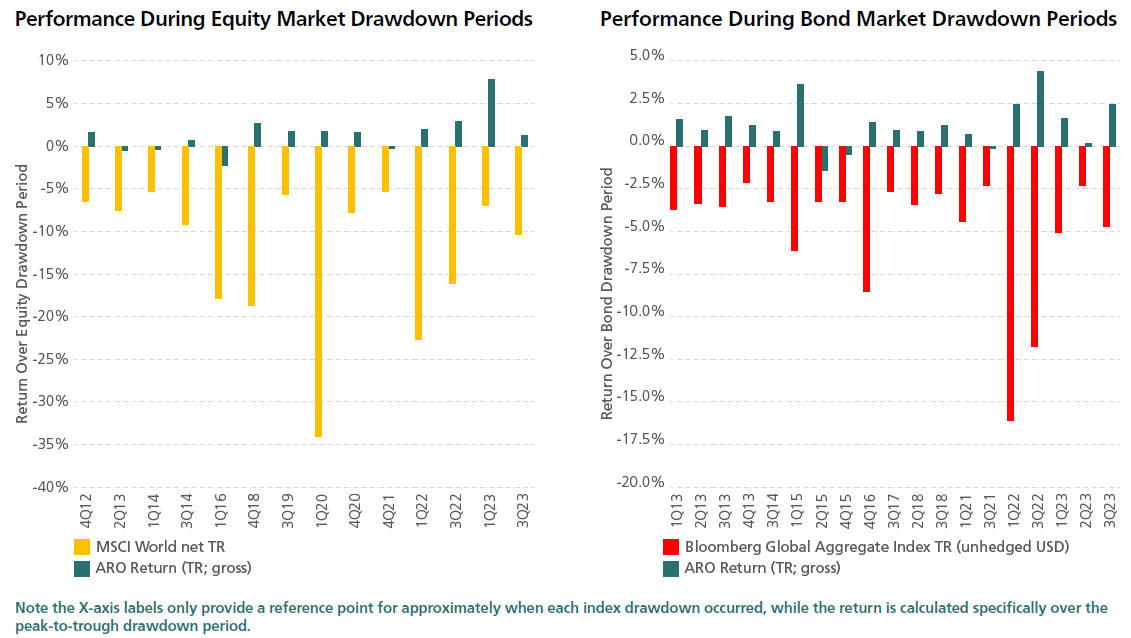

The absence of duration, corporate credit and foreign exchange risk (the portfolio is fully hedged) means that ARO works particularly well in providing downside protection during periods of market stress and improves risk-adjusted returns. In a conventional multi-asset portfolio diversification benefits, both performance and volatility, can be achieved by utilising the fund’s pure RV approach. The following charts highlight ARO’s performance during peak to trough drawdown periods.

To find out more about Ardea IM and ARO, please visit ardea.com.au.

*Ardea Real Outcome Fund was launched July 2012 and ActiveX Ardea Real Outcome Bond Fund (Managed Fund) (ASX:XARO) was launched December 2018.

Important Information

This material has been prepared by Ardea Investment Management Pty Limited (ABN 50 132 902 722 AFSL 329 828) (Ardea IM) the investment manager of the Ardea Real Outcome Fund (Fund). Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and is the responsible entity of the Fund. Other than information which is identified as sourced from Fidante in relation to the Fund, Fidante is not responsible for the information in this material, including any statements of opinion. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund’s Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Fund. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not a reliable indicator of future performance. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Ardea IM and Fidante have entered into arrangements in connection with the distribution and administration of financial products to which this material relates. In connection with those arrangements, Ardea IM and Fidante may receive remuneration or other benefits in respect of financial services provided by the parties. Fidante is not an authorised deposit-taking institution (ADI) for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante. Investments in the Fund are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group. D4-20231213